When the Renewal Bill Is Too Big for One Company to Carry: A Captive Conversation for HR and Finance

How group captives are giving mid-market employers a thirdoption between fully insured stability and self-funded volatility.

If this year's renewal letter landed harder than usual, the data backs up that instinct. Mercer projects a 6.5% average increase in total health benefit costs per employee for 2026 - the largest single-year jump since 2010, more than double the roughly 3% average annual increase the industry had grown used to over the prior decade.

Without any plan changes, Mercer estimates the increase would have approached 9% - meaning the 6.5%figure already reflects cost-shifting and benefit trims employers made just to soften the blow.

Other forecasters tell a similar story from different angles: Aon projects average employer health costs will surpass $17,000 per employee in 2026, a 9.5% jump from 2025, and PwC expects medical trend to surge 8.5% for a third consecutive year. For small and mid-market groups specifically, renewal increases in the 8-15% range have become common, with some employers reporting hikes as steep as 50% on their medical line.

For HR leaders, this shows upas harder conversations with employees about cost-sharing. For CFOs, it shows up as a budget line that no longer behaves predictably year over year. Both functions are increasingly asking the same question: is there a funding structure that offers more control than a fully insured plan, without the full claims volatility of going self-funded alone?

For a growing number of mid-market employers, the answer is a captive.

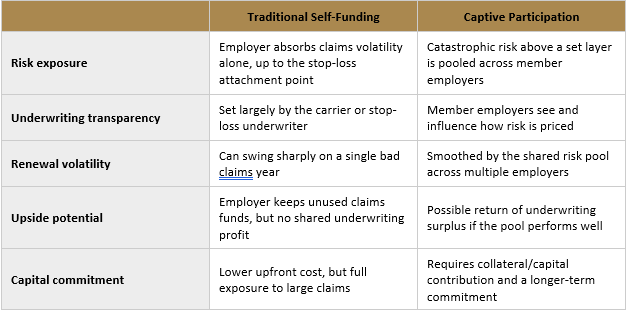

A captive is, at its core, an insurance company owned by the employers it covers. In the employee benefits context, a group of unrelated employers - often in similar industries, of similar size, or simply recruited by the same advisory firm - pool a defined layer of risk into a jointly owned entity. Each member typically remains self-funded for routine, predictable claims, but the captive absorbs claims that fall into a shared, mid-level risk band, with traditional stop-loss insurance still covering the most catastrophic claims above that.

The mechanics borrow from both worlds. Like self-funding, members keep day-to-day control over plan design, vendor selection, and claims data. Like a fully insured arrangement, members get protection from being wiped out by one bad claims year - but instead of paying a carrier for that protection, they're sharing it with other employers and, when the pool performs well, sharing in the underwriting return.

The defining feature isn’t the pooling itself - it’s the layered structure that splits cost, shared risk, and catastrophic protection into threedistinct tiers.

That three-layer structure is what distinguishes a captive from plain self-funding: a retained layer the employer funds directly, a shared layer pooled with other captive members, and a top stop-loss layer that caps exposure to truly catastrophic claims.

Three forces are pushing captives from a niche strategy into a mainstream renewal conversation.

Captives are not a free upgrade. Joining one is a multi-year commitment, not a one-renewal decision ,and most carry a required notice period or minimum participation term - this is not a structure to enter expecting to exit after a single rocky year.

There's also real capital and governance cost. Members typically post collateral and fund their layer of the shared risk pool upfront, which means a captive ties up cash that a fully insured employer wouldn't need to set aside. Some structures, particularly older “A/B fund” models retrofitted from property-and-casualty captives, ask employers to pre-fund both an individual layer and a shared layer, plus post collateral - worth scrutinizing closely, since that combination can leave an employer exposed for a large share of premium before stop-loss actually engages.

Governance is a genuine, ongoing commitment as well: captive members typically sit on a board or committee that reviews claims experience, underwriting decisions, and the performance of the shared pool. That's part of the value - it's real visibility most fully insured employers never get - but it does require HR and finance time that a fully insured renewal simply doesn't.

For employers who self-fund medical benefits in the U.S. and want to bring that coverage into a captive, there's a regulatory step worth planning for early: new captive arrangements that include medical coverage generally require approval from the Department of Labor, a process that can be time- and resource-intensive. Some employers manage this by starting outside the captive on traditional stop-loss while other welfare benefits (life, disability, dental) go in first, then folding medical in once the program and the relationship with regulators have matured.

A captive isn't the right next step for every group, and it isn't a substitute for the basic plan-performance work - claims review, stop-loss positioning, vendor evaluation - that should happen every renewal cycle regardless of funding structure. But for employers who are already self-funded, already carrying meaningful claims volatility, or facing a renewal that feels disconnected from their actual claims experience, it's worth a structured look rather than a passing mention.

A few questions worth raising before your next renewal:

These are exactly the kind of questions OVD is built to work through with you. The right funding strategy isn't a product we're selling - it's a conclusion we reach together, after looking honestly at your claims history, your risk tolerance, and where you want your benefits dollars working hardest. Whether a captive turns out to be the answer or not, that structured, no-pressure evaluation is the work we do every renewal. If your last renewal felt more like a number handed down than a strategy you helped shape, let's make this renewal different.

This article is intended for general informational purposes and does not constitute financial, legal, or actuarial advice. Employers considering a captive arrangement should consult with their broker, legal counsel, and actuarial advisors to evaluate suitability for their specific risk profile and goals.

Categories